March Market Update

March Recap

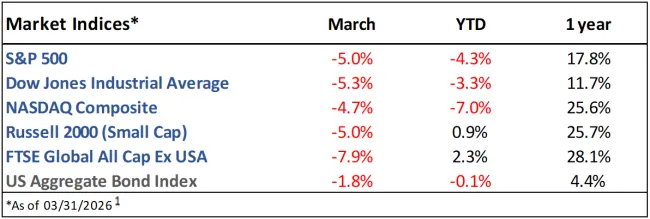

The S&P 500 fell -5.0% in March, ending the quarter down -4.3%, as the ongoing conflict with Iran weighed on markets. International equities fell more in March due to their heavy reliance on the Middle east for oil, though they are still outperforming U.S. equities in the 1-year and year-to-date time frames.1

The benchmark 10yr Treasury yield rose from 4.0% to 4.3% as surging oil prices pushed inflation expectations higher, leading to a -1.8% decline in the US Aggregate Bond Index.2

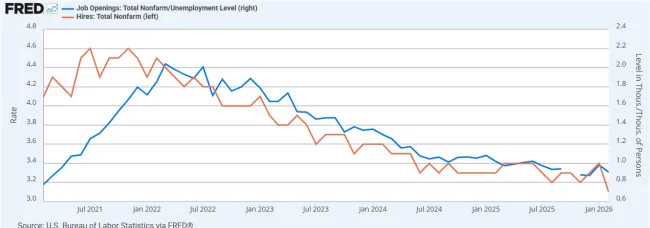

Inflation, measured by the Consumer Price Index (CPI), rose 3.3% year-over-year and a whopping 0.9% month-over-month, marking the fifth consecutive year above the Federal Reserve’s 2% target. Encouragingly, average wage growth has managed to keep up with inflation over that five-year period (figure 1). The economy added 178k jobs and the unemployment rate fell to 4.3%, some welcome positive news for a weakening labor market (figure 2).3

Current Developments (April)

Developments surrounding Iran and the closure of the Strait of Hormuz continue to be of major importance to the market. Recently, a 2-week ceasefire agreement between the U.S. and Iran kicked off an impressive rally for stocks, with the S&P 500 rebounding to all-time highs after having fallen over 9% from highs in late March.4

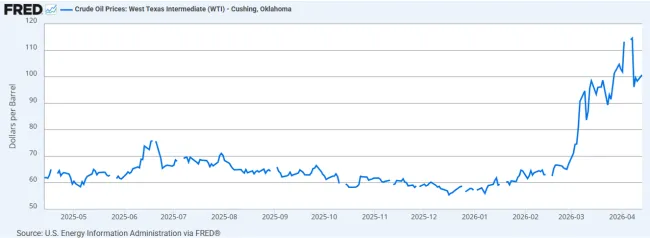

Thanks in part to this ceasefire, oil prices are now well off the highs from early April, though they remain up over 50% on the year (figure 3).

This drop in oil prices has led to a decline in Treasury yields and mortgage rates, though both remain higher since the beginning of the conflict.2

The Future

As we enter the second month of the conflict with Iran, we expect headlines to continue to drive market performance until a more permanent resolution is reached.

Due to rising yields and inflation expectations, the Federal Reserve is no longer expected to cut interest rates this year, a notable shift from the beginning of the year when two cuts were expected.5

Q1 earnings are expected to grow 13%, which would mark the sixth straight quarter of double-digit growth. For full-year 2026, earnings are expected to grow 18%, with all 11 S&P 500 sectors projected to post positive growth.6

Since 1950, April has produced an average return of nearly 1.5% for the S&P 500.7

1. https://ycharts.com/indices/%5ESPXTR, https://ycharts.com/indices/%5EDJITR, https://ycharts.com/indices/%5ENACTR, https://ycharts.com/indices/%5ERUTTR, https://ycharts.com/indices/%5EMSEAFETR, https://ycharts.com/indices/%5EBBUSATR – Index Performance

2. https://www.cnbc.com/bonds/ - Bond Yields

3. https://www.investing.com/economic-calendar/ - Economic data

4. https://www.bbc.com/news/articles/ce84z6y3ke4o - U.S/Iran ceasefire

5. https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html – Investor rate expectations

6. https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/Earnings Insight_041026A.pdf - Earnings expectations

7. https://www.visualcapitalist.com/charted-average-sp-500-return-by-month-since-1950/– Monthly market history

The Gasaway Team

7110 Stadium Drive

Kalamazoo, MI 49009

(269) 324-0080

FAX (269) 324-3834

The views expressed are those of the author as of the date noted, are subject to change based on market and other various conditions. This presentation is not an offer or a solicitation to buy or sell securities. The material discussed is meant to provide general education information only and it is not to be construed as specific investment, tax or legal advice and does not give investment recommendations.

Certain risks exist with any type of investment and should be considered carefully before making any investment decisions. Keep in mind that current and historical facts November not be indicative of future results.

Additional information, including management fees and expenses, is provided on our Form ADV Part 2 available upon request or at the SEC’s Investment Adviser Public Disclosure website, https://adviserinfo.sec.gov/firm/summary/123807.