May Market Update

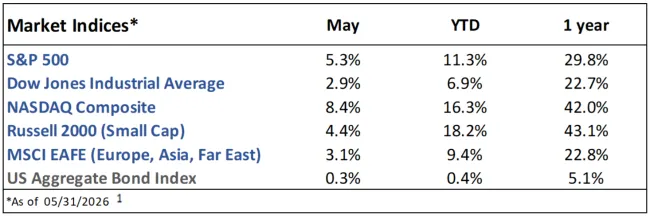

Market Indices Performance

May Recap

The S&P 500 rose 5.3% in May, continuing its recovery after a negative March. The tech-heavy Nasdaq outperformed for the second month in a row as AI enthusiasm, supported by strong earnings, propelled stocks higher. However, even with AI dominating the headlines, small caps have quietly been the best-performing sector this year.1

The benchmark 10yr Treasury yield ended the month where it started at 4.4% after spiking to 4.66% mid-month as inflation expectations surged higher.2

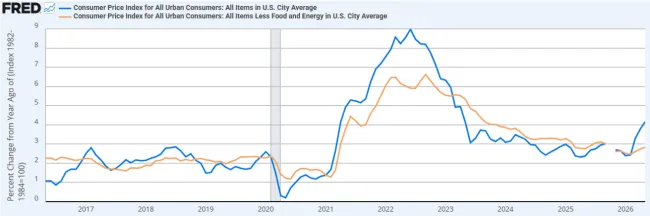

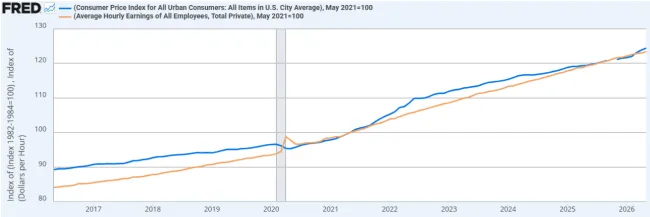

Inflation, measured by the Consumer Price Index (CPI), rose 4.2% year-over-year as energy prices remained elevated due to the war in Iran. Core inflation, which excludes food and energy prices, rose 2.9% year-over-year (Figure 1). Inflation has now been above the Federal Reserve’s 2% target for over five straight years. The economy added 172k jobs while the unemployment rate remained at 4.3%, marking the third straight report in which job growth exceeded expectations by at least 50k jobs. Average hourly earnings rose 3.4% year-over-year but have not managed to outpace inflation over the past 5 years (Figure 2).3

Q1 earnings season concluded with 28% growth, well above initial expectations of 13% earnings growth.4

Current Developments (June)

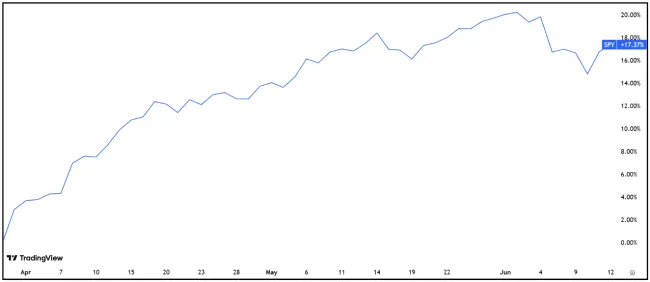

After an almost uninterrupted 20% rise in the S&P 500 from the end of March to the beginning of June, markets have pulled back slightly in June (as of June 12) (Figure 1). Despite being up just under 10% in 2026, the index’s P/E Ratio has actually declined as the strength in earnings growth has outpaced these gains in price.5

The long awaited, record-breaking SpaceX initial public offering (IPO) took place on June 12, raising $75 billion (the previous record was $38 billion). It quickly rose to a market capitalization of over $2 trillion, making it the 6th most valuable company in the world behind only Amazon, Microsoft, Apple, Google, and Nvidia.6 Not to be outdone, Google announced an $80 billion equity offering to fund further AI spending.7

The ceasefire between the U.S. and Iran remains in place, and President Trump has shared many times that a resolution is close.

The Future

We still expect the conflict with Iran to influence the market, especially its impact on oil prices and the resulting upward pressure on inflation and bond yields.

The Federal Reserve will meet on June 16-17, which will mark Kevin Warsh’s first meeting and press conference as Chair. With inflation rising back above 4% after several rate cuts, he and the rest of the FOMC face a difficult policy decision and an equally difficult message to communicate.

Speaking of the Federal Reserve, investors now expect one rate hike in 2026 after beginning the year forecasting two cuts.8

For Q3, investors expect 25% earnings growth, which would mark the 7th straight quarter of double-digit growth. For full-year 2026, earnings are now expected to grow 23%.4

Since 1950, June has produced a mediocre average return of 0.1% for the S&P 500.9

1. https://ycharts.com/indices/%5ESPXTR, https://ycharts.com/indices/%5EDJITR, https://ycharts.com/indices/%5ENACTR, https://ycharts.com/indices/%5ERUTTR, https://ycharts.com/indices/%5EMSEAFETR, https://ycharts.com/indices/%5EBBUSATR – Index Performance

2. https://www.cnbc.com/bonds/ - Bond Yields

3. https://www.investing.com/economic-calendar/ - Economic data

4. https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/Earnings Insight_051526.pdf- Earnings

5. https://www.macrotrends.net/2577/sp-500-pe-ratio-price-to-earnings-chart- S&P 500 PE Ratio

6. https://www.reuters.com/graphics/SPACEX-IPO/byprdokrkpe/- SpaceX IPO

7. https://www.reuters.com/legal/transactional/alphabet-raise-8475-billion-upsized-equity-offering-fund-ai-ambitions-2026-06-03/ - Google equity offering

8. https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html - Investor rate expectations

9. https://www.visualcapitalist.com/charted-average-sp-500-return-by-month-since-1950/– Monthly market history

The Gasaway Team

7110 Stadium Drive

Kalamazoo, MI 49009

(269) 324-0080

FAX (269) 324-3834

The views expressed are those of the author as of the date noted, are subject to change based on market and other various conditions. This presentation is not an offer or a solicitation to buy or sell securities. The material discussed is meant to provide general education information only and it is not to be construed as specific investment, tax or legal advice and does not give investment recommendations.

Certain risks exist with any type of investment and should be considered carefully before making any investment decisions. Keep in mind that current and historical facts not be indicative of future results.

Additional information, including management fees and expenses, is provided on our Form ADV Part 2 available upon request or at the SEC’s Investment Adviser Public Disclosure website, https://adviserinfo.sec.gov/firm/summary/123807.