July Market Update

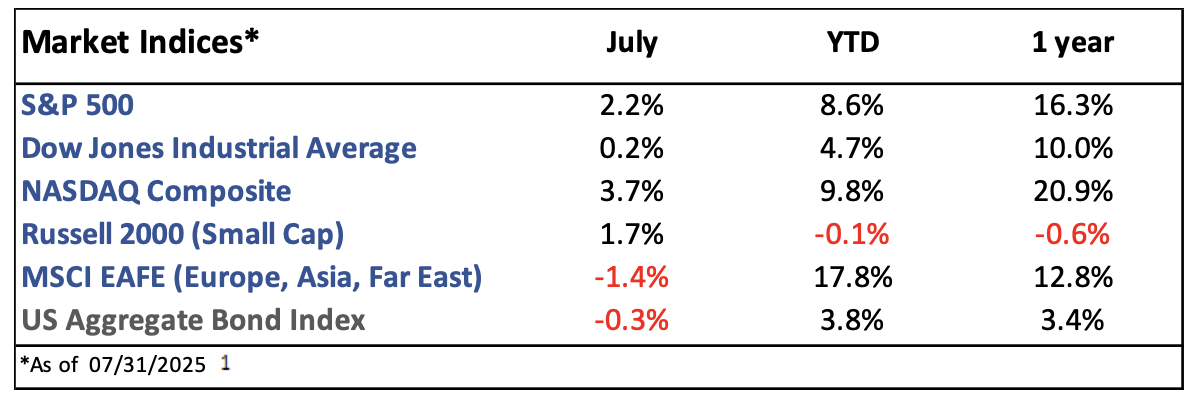

Market Indices Performance

July Recap

The S&P 500 rose 2.2% in July, its third straight positive month after three straight negative months.1 International equities continued to underperform after outperforming earlier in the year, as positive earnings announcement for U.S. stocks have continued to drive domestic prices higher. Bond yields ended the month roughly where they started, dipping late in the month after a weak jobs report signaled concerns for long-term growth.²

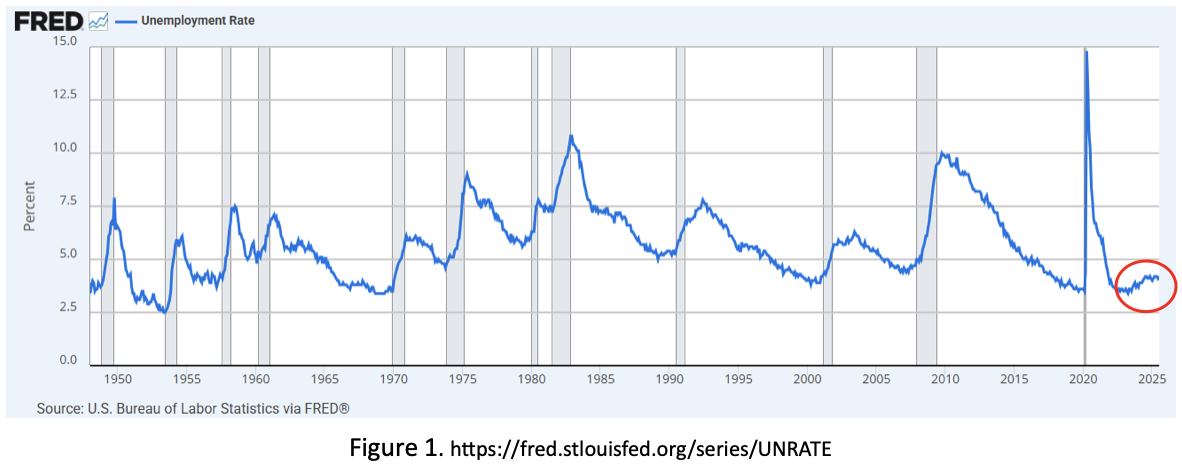

Inflation, measured by the Consumer Price Index (CPI), rose 2.7% year-over-year, marking the 52nd consecutive month above the Federal Reserve’s 2% target.3 The labor market has started to show some cracks: employers added fewer jobs than expected (73k vs 106k) and the previous two reports were revised down by a whopping 250k jobs. The unemployment rate remained steady, ticking up to 4.2%; it has remained below 4.5% since 2021, which is well below the historical average (see figure 1).⁴ The ratio of job openings to unemployed people continues to hover around 1.⁵

President Trump signed the “One Big Beautiful Bill” into law over the 4th of July weekend. It permanently extends the individual income tax brackets set in 2017, allows deductions for tips, overtime pay, and those over 65 years old, and establishes “Trump accounts” - savings accounts for children born between 2025 and 2028, each initially funded with a $1,000 government contribution into a selected investment. Whie these tax breaks and spending cuts are projected to boost GDP, the act is still expected to add ~$3.5 trillion to the federal deficit.⁶

Current Developments (August)

President Trump’s increased reciprocal tariff rates went into effect on August 7. Since April, markets have grown less reactive to tariff headlines, seemingly choosing instead to wait for real data from the tariffs before reacting. A trade deal with China has been postponed for another 90 days, while deals with other large economies like Japan and the EU have been finalized and include commitments for significant investment in the U.S.⁷

As the end of Q2 earnings season approaches, growth is tracking around 12%, well above the 5% expected at the start of the quarter.⁸ GDP grew by 3% in Q2 after contracting in Q1.⁹ Both consumer and producer price inflation were higher than expected in August, slightly lowering the odds of a rate cut in September.¹⁰

The Future

Following what is shaping up to be a strong Q2 earnings season, analysts expect 10% earnings growth for the S&P 500 in 2025.8 August tends to be a mediocre month for stocks and has historically marked the start of a challenging three-month stretch for markets.12

Both Wall Street and the Federal Reserve continue to anticipate

two interest rate cuts in 2025.10,11

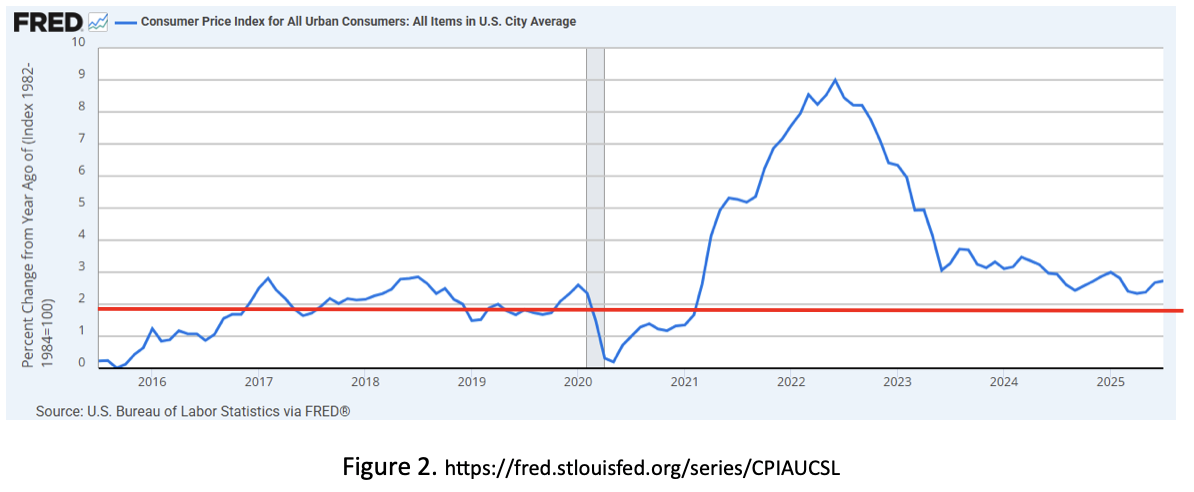

President Trump, however, has continued to call for the Federal Reserve to cut rates by over 1% to lower borrowing costs for consumers and refinancing costs for the Treasury. Potential tariff-driven price hikes and inflation remaining well above the 2% target have made the Fed hesitant to cut rates (see figure 2).

1. https://ycharts.com/indices/%5ESPXTR, https://ycharts.com/indices/%5EDJITR, https://ycharts.com/indices/%5ENACTR, https://ycharts.com/indices/%5ERUTTR, https://ycharts.com/indices/%5EMSEAFETR, https://ycharts.com/indices/%5EBBUSATR – Index Performance

2. https://www.cnbc.com/quotes/US10Y/- 10yr Treasury Yield

3. https://www.investing.com/economic-calendar/cpi-733- CPI

4. https://www.investing.com/economic-calendar/nonfarm-payrolls-227 - Jobs reports

5. https://fred.stlouisfed.org/series/JTSJOL- Job openings

6. https://taxfoundation.org/research/all/federal/trump-tariffs-trade-war/- Tariff tracker

7. https://www.wealthenhancement.com/blog/one-big-beautiful-tax-bill - Big Beautiful Bill

8. https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_071125.pdf - Earnings

9. https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html – Investor rate expectations

10. https://www.jpmorgan.com/insights/outlook/economic-outlook/fed-meeting-June-2025- Fed Outlook

11. https://www.nasdaq.com/articles/heres-the-average-stock-market-return-in-every-month-of-the-year – Monthly market history

12. https://www.atlantafed.org/cqer/research/gdpnow- Q2 GDP

The Gasaway Team

7110 Stadium Drive

Kalamazoo, MI 49009

(269) 324-0080

FAX (269) 324-3834

The views expressed are those of the author as of the date noted, are subject to change based on market and other various conditions. This presentation is not an offer or a solicitation to buy or sell securities. The material discussed is meant to provide general education information only and it is not to be construed as specific investment, tax or legal advice and does not give investment recommendations.

Certain risks exist with any type of investment and should be considered carefully before making any investment decisions. Keep in mind that current and historical facts may not be indicative of future results.

Additional information, including management fees and expenses, is provided on our Form ADV Part 2 available upon request or at the SEC’s Investment Adviser Public Disclosure website, https://adviserinfo.sec.gov/firm/summary/123807.

This material was created for educational and informational purposes only and is not intended as ERISA, tax, legal, or investment advice. If you are seeking investment advice specific to your needs, such advice services must be obtained on your own separate from this educational material. ©401(k) Marketing, LLC. All rights reserved. Proprietary and confidential. Do not copy or distribute outside original intent.