September Market Update

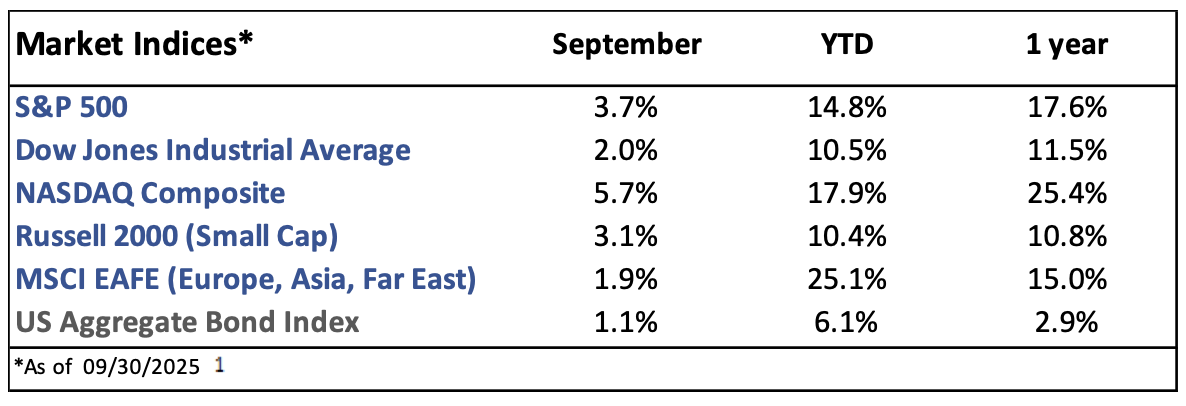

Market Indices Performance

September Recap

The S&P 500 rose 3.7% in September, hitting several new all-time highs and marking its fifth straight positive month.1 Big Tech stocks led the gains on the back of strong earnings and continued AI development. The benchmark 10yr Treasury yield ended lower, finally breaking below the 4.2% level as investors now expect three total rate cuts in 2025.2

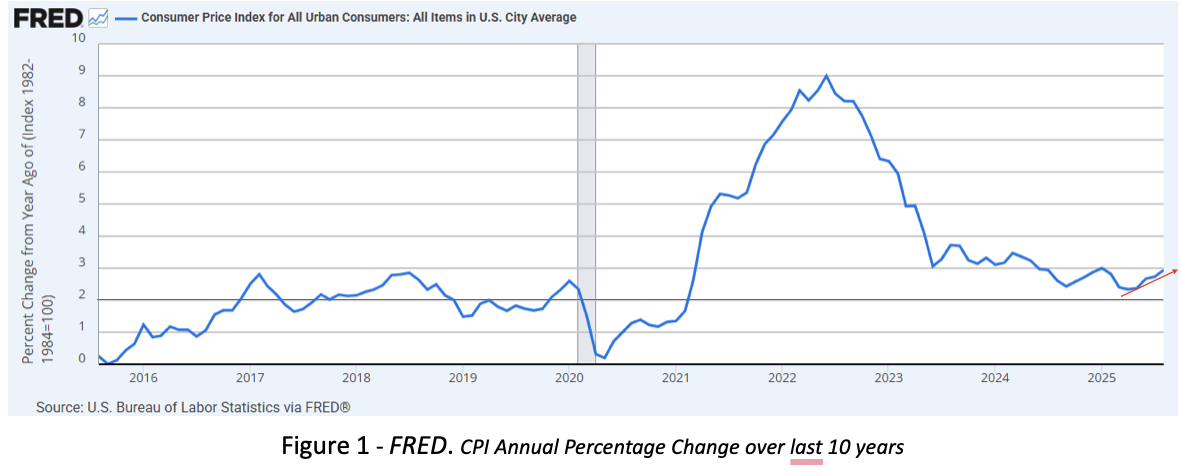

Due to the ongoing government shutdown, September’s inflation and labor market reports have been delayed. Expectations are for 3.1% inflation, 40k jobs added, and the unemployment rate remaining at 4.3%.3 This would send inflation back above 3% for the first time since May 2024, another setback given that price growth has remained above the Federal Reserve’s 2% target for more than four and a half years now (figure 1).

The Federal Reserve delivered the first rate cut of 2025 on the 17th, with Chair Jerome Powell characterizing the move as a ‘risk-management cut’ in the face of a weakening labor market.4

Current Developments (October)

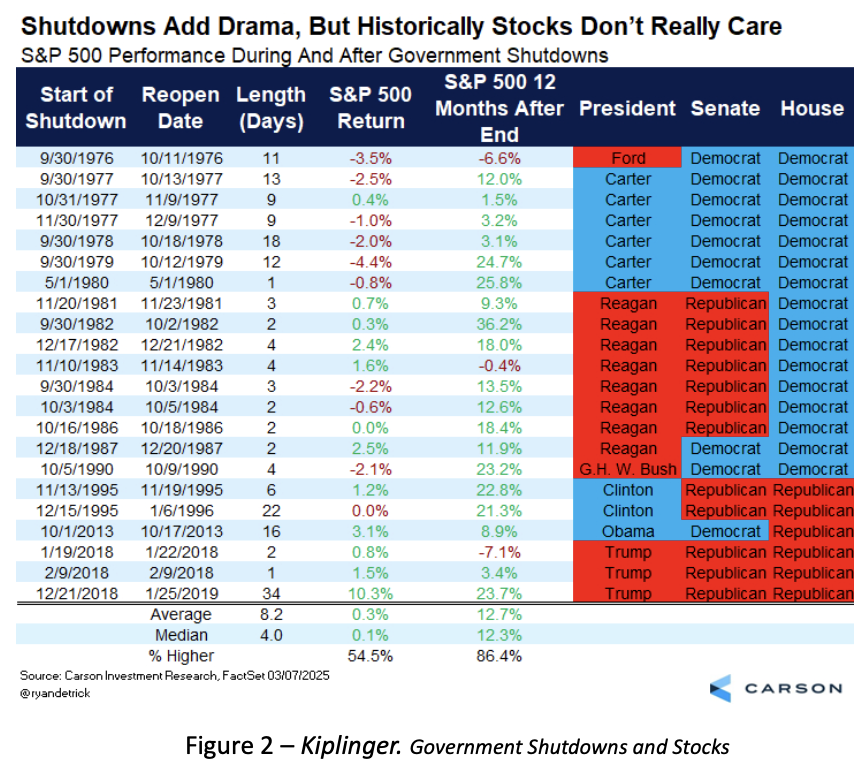

On October 1, the government shut down over disagreements regarding healthcare funding. As of day 14, it has already become the 5th longest shutdown since 1976.5 Despite the political noise, stocks have historically held up well during shutdowns and performed even better afterwards (figure 2).

President Trump recently threated 100% tariffs on China following China’s announcement of further rare earth export controls.6 Markets initially dropped on the news but rebounded after Trump hinted that a deal is likely to be reached before the November 1 deadline.

A baseline 10% tariff and tariffs on key trading partners like Canada (35%), Mexico (25%), India (50%), and Brazil (50%) remain in effect, while deals including 15% tariffs on most goods have been struck with Japan and the EU.7

The Future

After another quarter of double-digit earnings growth in Q2, S&P 500 earnings are expected to rise 8% in Q3.8 October is historically a mediocre month for stocks, but November and December typically deliver strong gains.9

Both Wall Street and the Federal Reserve continue to project two additional interest rate cuts in 2025, following the one in September.10 This would bring the federal funds rate down to a range of 3.50%-3.75% by the end of the year.

1. https://ycharts.com/indices/%5ESPXTR, https://ycharts.com/indices/%5EDJITR, https://ycharts.com/indices/%5ENACTR, https://ycharts.com/indices/%5ERUTTR, https://ycharts.com/indices/%5EMSEAFETR, https://ycharts.com/indices/%5EBBUSATR – Index Performance

2. https://www.cnbc.com/bonds/ - Bond Yields

3. https://www.investing.com/economic-calendar/ - Economic data

4. https://www.cnbc.com/2025/09/17/fed-rate-decision-september-2025.html - Fed rate cut

5. https://www.ncsl.org/in-dc/federal-government-shutdown-what-it-means-for-states-and-programs- Government Shutdowns

6. https://www.theguardian.com/us-news/2025/oct/14/china-us-world-economy-trump-tariffs – China Tariffs

7. https://www.atlanticcouncil.org/programs/geoeconomics-center/trump-tariff-tracker/ - Tariffs

8. https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_101025.pdf - Earnings

9. https://www.nasdaq.com/articles/heres-the-average-stock-market-return-in-every-month-of-the-year – Monthly market history

10. https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html – Investor rate expectations

The Gasaway Team

7110 Stadium Drive

Kalamazoo, MI 49009

(269) 324-0080

FAX (269) 324-3834

The views expressed are those of the author as of the date noted, are subject to change based on market and other various conditions. This presentation is not an offer or a solicitation to buy or sell securities. The material discussed is meant to provide general education information only and it is not to be construed as specific investment, tax or legal advice and does not give investment recommendations.

Certain risks exist with any type of investment and should be considered carefully before making any investment decisions. Keep in mind that current and historical facts may not be indicative of future results.

Additional information, including management fees and expenses, is provided on our Form ADV Part 2 available upon request or at the SEC’s Investment Adviser Public Disclosure website, https://adviserinfo.sec.gov/firm/summary/123807.

This material was created for educational and informational purposes only and is not intended as ERISA, tax, legal, or investment advice. If you are seeking investment advice specific to your needs, such advice services must be obtained on your own separate from this educational material. ©401(k) Marketing, LLC. All rights reserved. Proprietary and confidential. Do not copy or distribute outside original intent.